Semiconductor Foundry Market

Semiconductor Foundry Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700957 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

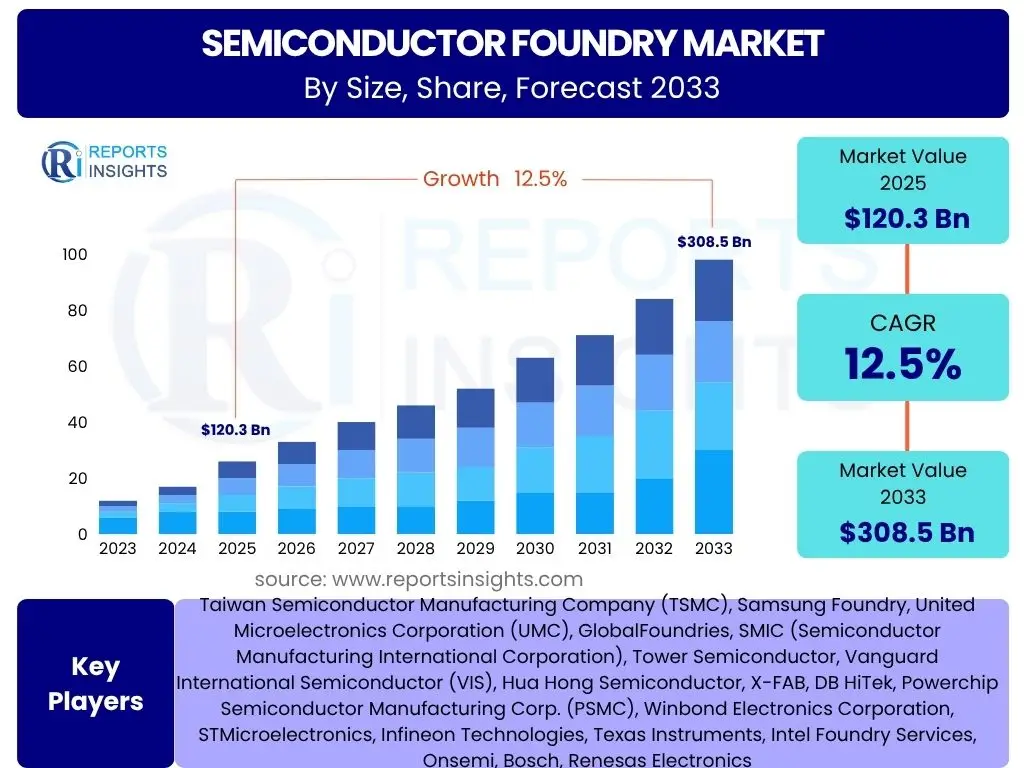

Semiconductor Foundry Market Size

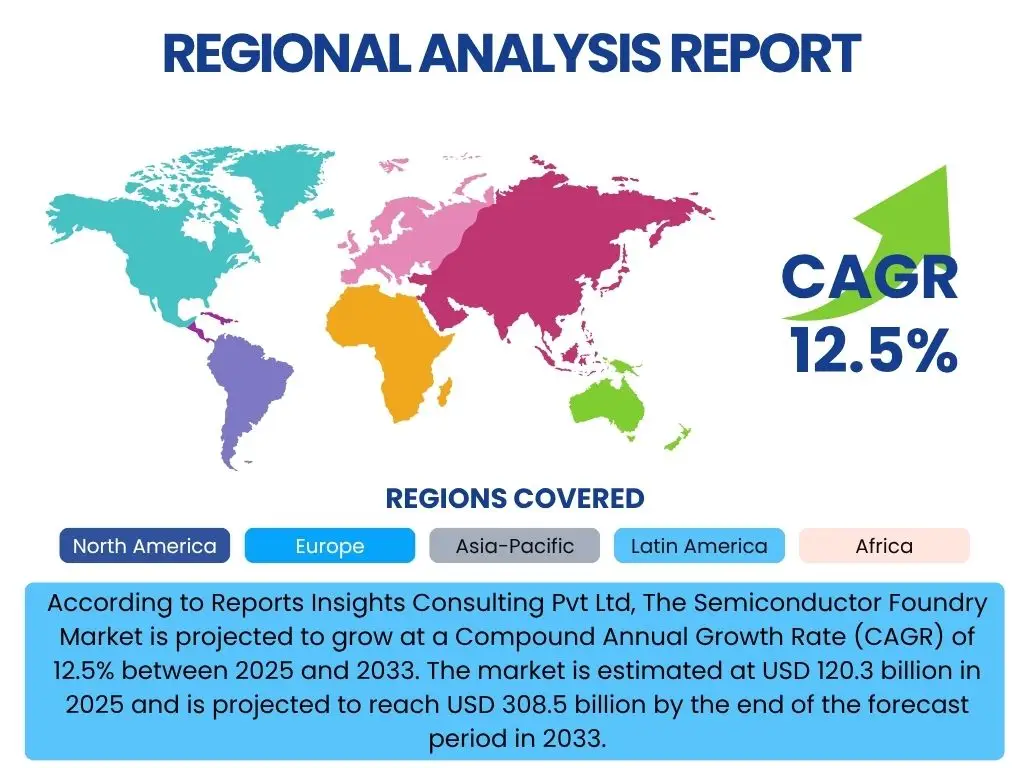

According to Reports Insights Consulting Pvt Ltd, The Semiconductor Foundry Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 120.3 billion in 2025 and is projected to reach USD 308.5 billion by the end of the forecast period in 2033.

Key Semiconductor Foundry Market Trends & Insights

The semiconductor foundry market is currently experiencing dynamic shifts driven by escalating demand for advanced chip technologies and evolving global supply chain strategies. Users frequently inquire about the primary forces shaping this industry, including technological advancements, geopolitical influences, and shifts in manufacturing paradigms. A notable trend is the relentless pursuit of smaller process nodes, essential for high-performance computing (HPC), artificial intelligence (AI), and next-generation mobile devices. This trend necessitates colossal investments in research and development, alongside highly sophisticated manufacturing capabilities, pushing the boundaries of what is technologically feasible.

Beyond miniaturization, significant interest surrounds the diversification of global semiconductor manufacturing footprints. Geopolitical considerations are increasingly influencing investment decisions, leading to new fab construction in regions traditionally less prominent in advanced semiconductor production, such as North America and Europe. This push for regional self-sufficiency aims to enhance supply chain resilience and reduce reliance on concentrated manufacturing hubs. Furthermore, the market is witnessing a surge in demand for specialized chips tailored for specific applications, alongside the growing adoption of advanced packaging technologies like chiplets and 3D stacking, which are crucial for achieving higher performance and power efficiency in complex systems.

The industry is also grappling with environmental sustainability, with foundries investing in energy-efficient processes and cleaner manufacturing techniques. This reflects a broader industry commitment to reducing carbon footprints and adhering to stricter environmental regulations. These combined trends highlight a market that is not only expanding rapidly in terms of volume and value but also undergoing fundamental transformations in its operational, strategic, and geographic dimensions.

- Advanced Node Dominance: Increasing demand for 7nm, 5nm, and sub-5nm process technologies for high-performance applications.

- Geopolitical Influence & Supply Chain Resiliency: Governments and companies investing in localized manufacturing to reduce dependency and enhance security.

- AI and High-Performance Computing (HPC) Demand: Exponential growth in AI accelerators and data center chips driving advanced wafer starts.

- Advanced Packaging Solutions: Rising adoption of 2.5D/3D packaging and chiplet architectures for performance and integration.

- Sustainability Initiatives: Focus on energy efficiency, water conservation, and green manufacturing practices in fab operations.

- Automotive Semiconductor Growth: Increasing silicon content in electric vehicles (EVs) and autonomous driving systems.

- Specialized Chip Development: Proliferation of application-specific integrated circuits (ASICs) and custom silicon solutions.

AI Impact Analysis on Semiconductor Foundry

User queries regarding the impact of Artificial Intelligence (AI) on the Semiconductor Foundry sector predominantly focus on its dual role: as a significant driver of chip demand and as a transformative force in foundry operations. AI's insatiable appetite for computational power is directly fueling the need for highly specialized and advanced chips, including Graphics Processing Units (GPUs), Application-Specific Integrated Circuits (ASICs), and Field-Programmable Gate Arrays (FPGAs), all requiring fabrication on the most cutting-edge process nodes. This translates into substantial revenue streams for foundries capable of producing these complex, high-performance components, making AI one of the most critical demand-side catalysts for the industry's current growth trajectory.

Beyond driving demand, AI is revolutionizing the internal workings of semiconductor foundries. Users are keenly interested in how AI enhances efficiency, reduces costs, and improves quality in an inherently complex manufacturing environment. AI and machine learning algorithms are being deployed across various stages of the manufacturing process, from predictive maintenance of sophisticated machinery to optimizing yield rates and defect detection. By analyzing vast datasets generated during production, AI can identify patterns, predict equipment failures before they occur, and pinpoint sources of anomalies, significantly reducing downtime and waste.

Furthermore, AI is increasingly integrated into Electronic Design Automation (EDA) tools, accelerating the design cycle for complex chips and enabling more efficient verification. This not only streamlines the pre-production phase but also ensures that designs are optimized for manufacturability, leading to higher yields and reduced iterations. The strategic adoption of AI within foundries promises to unlock new levels of automation, precision, and operational intelligence, reinforcing the industry's capacity to meet future technological demands while navigating increasing complexities.

- Increased Demand for Advanced AI Chips: AI/ML accelerators, GPUs, and specialized ASICs drive significant wafer orders at leading nodes.

- Optimized Manufacturing Processes: AI-powered predictive maintenance, anomaly detection, and real-time process control enhance fab efficiency.

- Improved Yield Management: Machine learning algorithms analyze production data to identify defect patterns and optimize yield rates.

- Accelerated Electronic Design Automation (EDA): AI tools reduce design cycle times and improve chip verification processes.

- Automation of Quality Control: AI-driven inspection systems provide faster and more accurate defect identification.

- Intelligent Supply Chain Management: AI optimizes inventory, logistics, and material flow within foundry operations.

Key Takeaways Semiconductor Foundry Market Size & Forecast

Common user inquiries about the Semiconductor Foundry market size and forecast often center on understanding the primary growth engines, the long-term sustainability of demand, and the underlying technological shifts. A key insight is the market's robust growth trajectory, propelled significantly by an insatiable global appetite for digital transformation and advanced computing. This includes the widespread adoption of AI, 5G connectivity, IoT devices, and increasingly sophisticated automotive electronics. Foundries, particularly those at the forefront of advanced process nodes, are strategically positioned to capitalize on these trends, becoming indispensable partners in the digital economy.

Another crucial takeaway is the deepening strategic importance of semiconductor manufacturing on a global scale. The forecast indicates sustained expansion, yet it also highlights the intensified geopolitical competition and national efforts to secure domestic chip supply chains. This translates into massive government incentives and private investments flowing into new fab construction and capacity expansion in diverse geographies, aiming to balance efficiency with resilience. While Asia Pacific remains the dominant manufacturing hub, North America and Europe are actively pursuing greater self-sufficiency in chip production, especially for critical applications.

Finally, the market's future growth is intrinsically linked to continuous innovation and substantial capital expenditure. The move towards smaller nodes, advanced packaging, and novel materials demands unprecedented levels of investment in R&D and manufacturing infrastructure. The ability of foundries to manage escalating complexity, maintain high yields, and attract skilled talent will be paramount in sustaining the projected growth. The market is not merely expanding; it is evolving structurally and technologically, presenting both lucrative opportunities and significant challenges for stakeholders.

- Strong Growth Trajectory: Market size projected to more than double by 2033, reflecting sustained demand across diverse applications.

- Advanced Nodes as Growth Drivers: Sub-7nm technologies are the primary revenue drivers, fueled by AI, HPC, and premium mobile devices.

- Geopolitical Influence & Regionalization: Increased investment in fab construction outside traditional hubs to enhance supply chain resilience.

- Capital-Intensive Nature: Continuous heavy investment in R&D and new equipment is critical for competitive advantage.

- Diversified End-Use Adoption: Growth driven by consumer electronics, automotive, industrial, and data center segments.

- Innovation Imperative: Success hinges on continuous technological advancement and efficient high-volume manufacturing.

Semiconductor Foundry Market Drivers Analysis

The semiconductor foundry market's expansion is fundamentally propelled by the pervasive digitalization across industries and the escalating demand for advanced electronic devices. The proliferation of Artificial Intelligence, High-Performance Computing, 5G technology, and the Internet of Things creates an insatiable need for more powerful, efficient, and specialized semiconductors. Foundries are at the core of enabling these technological advancements, providing the critical manufacturing backbone for chip designers. Additionally, the increasing complexity of modern chip designs necessitates reliance on specialized foundries that possess the expertise and vast capital to produce them, driving sustained demand for their services.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in AI/HPC applications | +3.0% | Global | Short-Medium Term (2025-2029) |

| Expansion of 5G and IoT ecosystems | +2.5% | Asia Pacific, Europe | Medium Term (2026-2030) |

| Increasing demand for automotive electronics | +2.0% | Global | Long Term (2027-2033) |

| Digital transformation across industries | +1.5% | North America, Europe | Short-Medium Term (2025-2029) |

| Government initiatives and subsidies | +1.0% | North America, Europe, Asia Pacific | Long Term (2025-2033) |

Semiconductor Foundry Market Restraints Analysis

Despite its robust growth trajectory, the semiconductor foundry market faces significant restraints that can impact its overall expansion and profitability. The most prominent constraint is the extraordinarily high capital expenditure required to establish and maintain state-of-the-art fabrication facilities (fabs). Building a new leading-edge fab can cost tens of billions of dollars, and the continuous need for upgrading equipment and processes to keep pace with technological advancements represents an ongoing, massive financial burden. This high barrier to entry limits the number of players and exacerbates the risk associated with market fluctuations.

Geopolitical tensions and trade disputes also pose substantial restraints. National security concerns and a desire for supply chain independence have led to restrictive trade policies, export controls, and increased scrutiny over cross-border investments, particularly between major economic blocs. Such measures can disrupt established supply chains, increase operational costs, and limit access to critical technologies or markets. Furthermore, the industry is highly susceptible to economic downturns, as demand for electronic devices can fluctuate significantly with global economic conditions, leading to cycles of oversupply or undersupply that impact foundry utilization rates and pricing power.

Another persistent restraint is the global shortage of skilled labor, particularly engineers and technicians with expertise in advanced semiconductor manufacturing. The highly specialized nature of the work requires extensive training, and the pipeline of qualified professionals struggles to meet the rapidly expanding needs of the industry. This shortage can lead to increased labor costs, delays in fab ramp-ups, and a constraint on innovation, challenging the industry's capacity to execute its ambitious expansion plans and maintain its technological edge.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital expenditure and R&D costs | -2.0% | Global | Long Term (2025-2033) |

| Geopolitical tensions and trade policies | -1.5% | Global | Short-Medium Term (2025-2029) |

| Supply chain vulnerabilities | -1.0% | Global | Short Term (2025-2027) |

| Skilled labor shortage | -0.8% | Global | Medium Term (2026-2030) |

Semiconductor Foundry Market Opportunities Analysis

The semiconductor foundry market is ripe with opportunities driven by both technological advancements and strategic geopolitical shifts. One significant area of opportunity lies in the continued proliferation of specialized chip designs that cater to niche but high-growth markets, such as quantum computing, advanced photonics, and customized AI accelerators. As system-on-chip (SoC) integration becomes increasingly complex, companies are opting for bespoke silicon solutions, creating a consistent demand for advanced foundry services capable of handling highly specific and intricate designs. This trend allows foundries to diversify their client base beyond traditional large chip designers and capture value from emerging technology ecosystems.

Another major opportunity stems from the global push for regional fab expansion and the accompanying government incentives. Countries and regions are committing substantial financial resources, including subsidies, tax breaks, and grants, to incentivize the construction of new fabrication plants within their borders. This strategic push, aimed at bolstering domestic supply chain resilience and technological sovereignty, creates fertile ground for foundries to expand their manufacturing footprint into new geographic areas. These initiatives not only reduce the financial burden of fab construction but also open access to new talent pools and regional markets, fostering long-term growth and diversification of operations.

Furthermore, the rapid evolution of advanced packaging solutions presents a lucrative opportunity. As traditional scaling laws (Moore's Law) face physical limitations, advanced packaging techniques like 2.5D and 3D integration, chiplets, and fan-out wafer-level packaging are becoming critical for achieving performance gains and power efficiency. Foundries that invest in these advanced packaging capabilities can offer more comprehensive solutions to their clients, integrating multiple dies into a single package to create heterogeneous systems. This vertical integration of services allows foundries to capture a larger share of the overall semiconductor value chain and differentiate themselves in a highly competitive market, catering to the growing demand for highly integrated and optimized solutions for next-generation applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of specialized chip designs (AI/ML, photonics) | +2.5% | Global | Medium Term (2026-2030) |

| Regional fab expansion and government incentives | +2.0% | North America, Europe | Long Term (2025-2033) |

| Advanced packaging solutions | +1.8% | Asia Pacific | Short-Medium Term (2025-2029) |

| Growth in compound semiconductors (SiC, GaN) | +1.5% | Global | Long Term (2027-2033) |

Semiconductor Foundry Market Challenges Impact Analysis

The semiconductor foundry market, while exhibiting robust growth, is confronted by several complex challenges that necessitate strategic navigation. A primary hurdle is the increasing difficulty and cost associated with maintaining high yield rates, especially for advanced process nodes. As transistor dimensions shrink to atomic scales, the manufacturing process becomes exquisitely sensitive to minute imperfections, making it challenging to achieve a high percentage of defect-free chips. Poor yields directly translate to higher production costs and reduced profitability, requiring continuous innovation in process control, metrology, and defect analysis to remain competitive.

Another significant challenge is the escalating complexity of semiconductor manufacturing itself. Each new generation of process technology introduces more intricate fabrication steps, requiring highly specialized and expensive equipment, such as Extreme Ultraviolet (EUV) lithography. This escalating complexity not only drives up capital expenditure but also increases the technical expertise required from the workforce and extends the time to market for new process nodes. Managing this complexity while simultaneously scaling production to meet global demand presents a formidable operational and engineering challenge for all foundries, particularly those at the leading edge.

Furthermore, the industry faces increasing pressure regarding environmental compliance and sustainability. Semiconductor manufacturing is resource-intensive, requiring vast amounts of water and energy, and generating various chemical byproducts. Stringent environmental regulations and growing societal expectations for corporate social responsibility compel foundries to invest significantly in greener manufacturing processes, water recycling, and renewable energy sources. While necessary for long-term viability, these investments add to operational costs and require continuous innovation to minimize environmental impact without compromising efficiency or competitiveness.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining high yield rates for advanced nodes | -1.5% | Global | Short-Medium Term (2025-2029) |

| Escalating manufacturing complexity | -1.2% | Global | Long Term (2025-2033) |

| Environmental compliance and sustainability pressures | -1.0% | Global | Medium Term (2026-2030) |

| Intellectual property protection | -0.7% | Global | Long Term (2025-2033) |

Semiconductor Foundry Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Semiconductor Foundry Market, offering a detailed understanding of its current landscape, historical performance, and future growth prospects. The scope encompasses a thorough examination of market size estimations, growth drivers, restraints, opportunities, and challenges influencing the industry's trajectory from 2025 to 2033. It delves into critical market trends, including technological advancements, geopolitical influences, and shifts in end-use application demand, providing strategic insights for stakeholders. The report also features extensive segmentation analysis across key parameters such as technology node, application, foundry type, and wafer size, along with regional breakdowns to highlight diverse market dynamics worldwide. Furthermore, a detailed profile of leading industry players offers competitive intelligence and an overview of their strategic positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 120.3 billion |

| Market Forecast in 2033 | USD 308.5 billion |

| Growth Rate | 12.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Foundry, United Microelectronics Corporation (UMC), GlobalFoundries, SMIC (Semiconductor Manufacturing International Corporation), Tower Semiconductor, Vanguard International Semiconductor (VIS), Hua Hong Semiconductor, X-FAB, DB HiTek, Powerchip Semiconductor Manufacturing Corp. (PSMC), Winbond Electronics Corporation, STMicroelectronics, Infineon Technologies, Texas Instruments, Intel Foundry Services, Onsemi, Bosch, Renesas Electronics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Semiconductor Foundry market is meticulously segmented to provide a granular view of its diverse dynamics, enabling stakeholders to identify specific growth areas and strategic opportunities. This segmentation allows for a comprehensive understanding of how different technological advancements, end-user demands, operational models, and manufacturing scales contribute to the overall market landscape. Analyzing these segments helps in pinpointing high-potential niches, assessing competitive advantages, and formulating targeted business strategies within the complex semiconductor ecosystem.

The primary segmentation axes include Technology Node, which differentiates foundries by their capability to produce chips at various transistor sizes, ranging from cutting-edge sub-7nm to mature 180nm+ processes. This categorization is crucial as it directly correlates with performance, power efficiency, and the cost of chip manufacturing. Application-based segmentation provides insights into the end-use industries driving demand, such as consumer electronics, automotive, telecommunications, and data processing, highlighting sector-specific needs and growth rates. Further segmentation by Foundry Type distinguishes between pure-play foundries, which exclusively offer manufacturing services, and Integrated Device Manufacturers (IDMs) that also provide foundry services alongside their own product lines. Lastly, Wafer Size segmentation (e.g., 300mm, 200mm) reflects the manufacturing capacity and efficiency, as larger wafers yield more chips per run, impacting cost and volume production capabilities. These detailed segmentations collectively paint a comprehensive picture of the market's structure and underlying drivers.

- By Technology Node:

- 7nm & below

- 10-16nm

- 20-28nm

- 40-65nm

- 90-180nm

- Above 180nm

- By Application:

- Consumer Electronics

- Automotive

- Telecommunications

- Data Processing

- Industrial

- Healthcare

- Others

- By Foundry Type:

- Pure-Play Foundries

- IDMs with Foundry Services

- By Wafer Size:

- 300mm

- 200mm

- 150mm & Below

Regional Highlights

The global Semiconductor Foundry market exhibits significant regional disparities, driven by varying investment levels, technological focuses, government policies, and demand concentrations. Each major region contributes uniquely to the market's dynamics, influencing global supply chains and technological advancement. Understanding these regional highlights is crucial for comprehensive market analysis and strategic decision-making.

- Asia Pacific (APAC): Dominates the global semiconductor foundry market, primarily due to the presence of leading pure-play foundries in Taiwan, South Korea, and China. This region is the manufacturing hub for advanced nodes and accounts for the largest share of global fab capacity. Significant investments in new fabs and R&D continue, driven by strong domestic demand for consumer electronics, telecommunications, and a growing AI ecosystem. Governments are actively supporting local semiconductor industries to enhance self-sufficiency and global competitiveness.

- North America: A key region for semiconductor design and innovation, North America is witnessing a resurgence in domestic manufacturing investments, spurred by government incentives such as the CHIPS Act. The focus is on increasing advanced node production capacity and securing critical supply chains for high-performance computing, AI, and defense applications. The region also benefits from a robust ecosystem of fabless design companies and strong R&D capabilities, driving demand for advanced foundry services.

- Europe: Europe is strategically investing in its semiconductor manufacturing capabilities, particularly for automotive, industrial, and specialized applications. Initiatives like the European Chips Act aim to double Europe's share in global semiconductor production, focusing on mature nodes and specific niche technologies. Collaborative efforts between industry, academia, and governments are fostering innovation in areas like power semiconductors, IoT, and embedded systems, diversifying the foundry landscape beyond traditional high-volume consumer chips.

- Latin America: While not a major manufacturing hub for advanced foundries, Latin America presents opportunities in assembly, test, and packaging (ATP) services. Growing domestic markets for consumer electronics and automotive components also drive demand for imported chips, creating potential for future regional fabrication growth or strategic partnerships in the long term.

- Middle East and Africa (MEA): This region is in the nascent stages of developing its semiconductor manufacturing capabilities, with emerging interest in localized production for specific applications such as smart infrastructure and energy. Significant investments in digital transformation and data centers across MEA are increasing demand for semiconductors, fostering opportunities for technology transfer and strategic collaborations with global foundries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Semiconductor Foundry Market.- Taiwan Semiconductor Manufacturing Company (TSMC)

- Samsung Foundry

- United Microelectronics Corporation (UMC)

- GlobalFoundries

- SMIC (Semiconductor Manufacturing International Corporation)

- Tower Semiconductor

- Vanguard International Semiconductor (VIS)

- Hua Hong Semiconductor

- X-FAB

- DB HiTek

- Powerchip Semiconductor Manufacturing Corp. (PSMC)

- Winbond Electronics Corporation

- STMicroelectronics

- Infineon Technologies

- Texas Instruments

- Intel Foundry Services

- Onsemi

- Bosch

- Renesas Electronics

Frequently Asked Questions

What is a semiconductor foundry?

A semiconductor foundry is a factory that manufactures integrated circuits (chips) for other companies, known as fabless semiconductor companies or integrated device manufacturers (IDMs). Foundries specialize in the highly complex and capital-intensive process of wafer fabrication, providing the manufacturing backbone for the global electronics industry.

What drives the growth of the semiconductor foundry market?

The growth of the semiconductor foundry market is primarily driven by increasing demand for advanced chips across various sectors, including artificial intelligence (AI), 5G telecommunications, high-performance computing (HPC), automotive electronics, and the Internet of Things (IoT). Geopolitical strategies also foster regional fab expansions to enhance supply chain resilience.

How does AI impact semiconductor foundries?

AI impacts semiconductor foundries in two key ways: it significantly increases the demand for high-performance AI-specific chips (e.g., GPUs, ASICs) that require leading-edge fabrication, and it optimizes foundry operations through AI-powered tools for predictive maintenance, yield management, and design automation (EDA).

What are the primary challenges facing semiconductor foundries?

Key challenges for semiconductor foundries include the extremely high capital expenditure required for advanced fabs, the escalating complexity and cost of manufacturing at smaller process nodes, the persistent global shortage of skilled labor, and geopolitical tensions influencing trade and supply chain stability.

Which regions are key players in the semiconductor foundry market?

Asia Pacific (particularly Taiwan, South Korea, and China) is the dominant region for semiconductor foundry manufacturing, holding the largest market share and advanced node capabilities. North America and Europe are also significant players, focusing on design innovation and increasing domestic production through strategic investments and government incentives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted