Commercial Refrigeration Equipment Market

Commercial Refrigeration Equipment Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707745 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

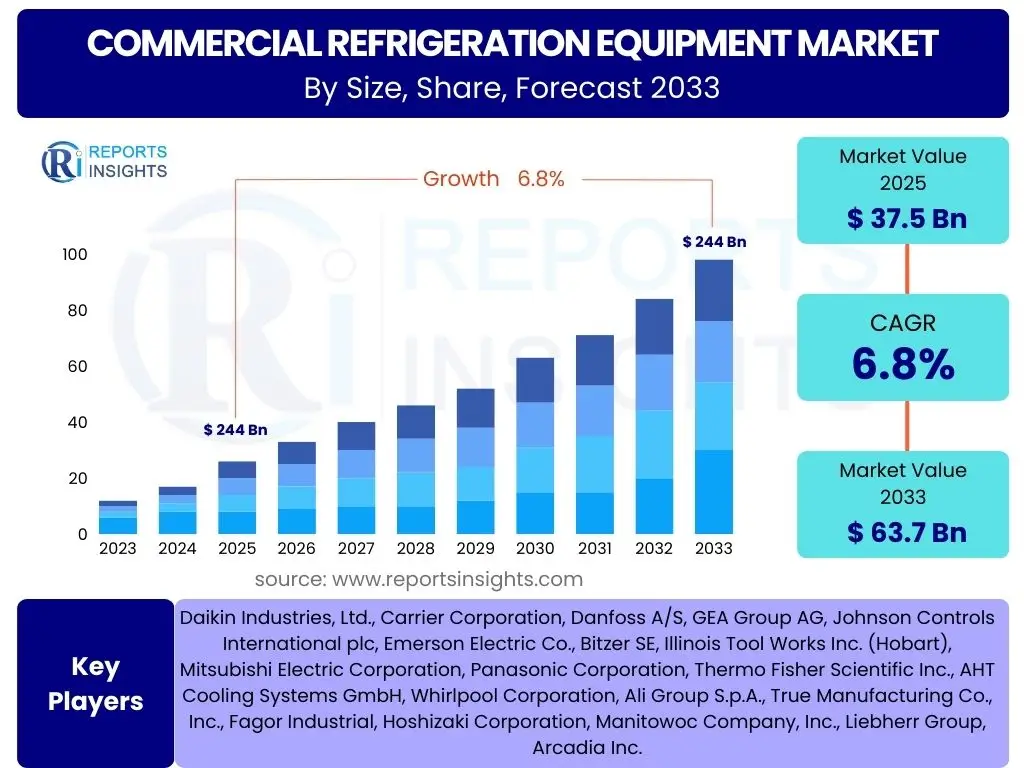

Commercial Refrigeration Equipment Market Size

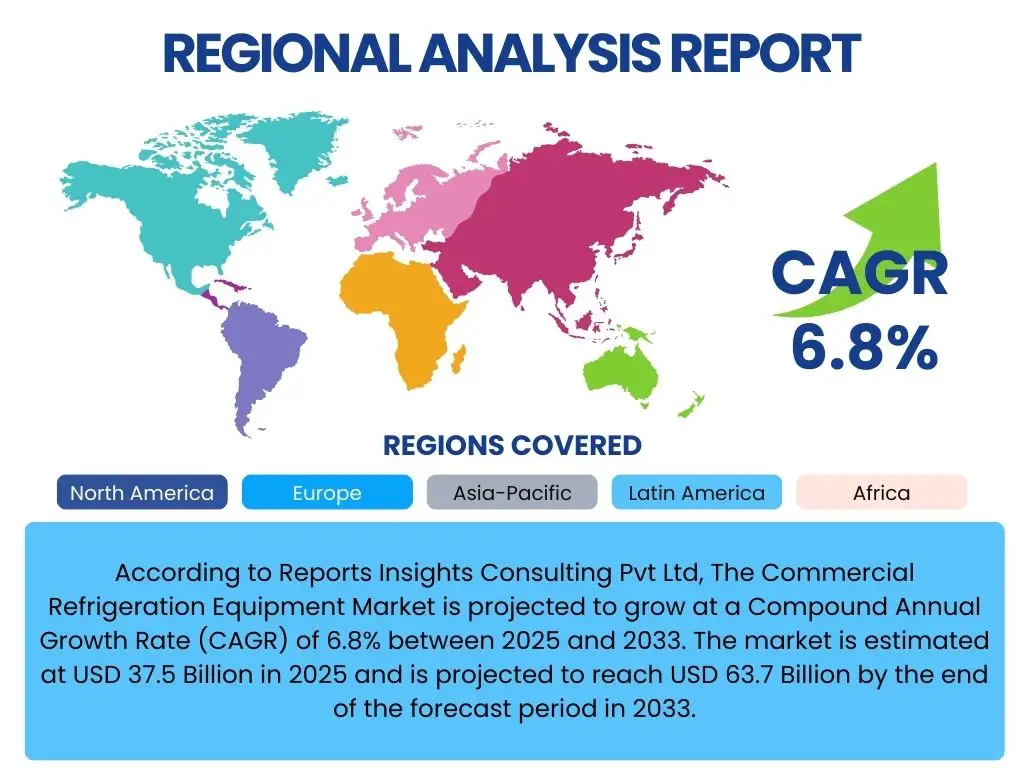

According to Reports Insights Consulting Pvt Ltd, The Commercial Refrigeration Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 37.5 Billion in 2025 and is projected to reach USD 63.7 Billion by the end of the forecast period in 2033.

Key Commercial Refrigeration Equipment Market Trends & Insights

The commercial refrigeration equipment market is currently undergoing significant transformation, driven by evolving consumer preferences, stringent environmental regulations, and technological advancements. A primary focus for businesses and consumers alike revolves around energy efficiency and sustainability. There is a strong demand for refrigeration units that consume less power and utilize environmentally friendly refrigerants, reflecting a global shift towards greener operations and a desire to reduce operational costs. This trend is further amplified by the increasing adoption of smart technologies that enhance performance monitoring and predictive maintenance, allowing for more efficient management of refrigeration assets.

Another crucial trend influencing the market is the rapid expansion of the food service and retail sectors, particularly in emerging economies. The growing demand for fresh and frozen foods, coupled with the proliferation of supermarkets, convenience stores, and quick-service restaurants, necessitates robust and reliable refrigeration infrastructure. Additionally, the development of cold chain logistics, from farm to fork, continues to be a pivotal area of investment, ensuring product quality and safety across various stages of distribution. Customization and modular designs are also gaining traction, enabling businesses to tailor refrigeration solutions to their specific operational needs and space constraints.

- Growing emphasis on energy-efficient refrigeration solutions.

- Increasing adoption of natural and low-GWP refrigerants.

- Integration of smart technologies and IoT for enhanced monitoring.

- Expansion of cold chain infrastructure, especially in developing regions.

- Rising demand from organized food retail and foodservice sectors.

- Shift towards modular and customized refrigeration systems.

AI Impact Analysis on Commercial Refrigeration Equipment

Artificial Intelligence (AI) is set to revolutionize the commercial refrigeration equipment sector by introducing unprecedented levels of efficiency, predictive capabilities, and operational intelligence. Users frequently inquire about how AI can optimize energy consumption, reduce maintenance costs, and improve overall system reliability. AI algorithms can analyze vast amounts of data from sensors embedded in refrigeration units, including temperature fluctuations, compressor cycles, and door openings, to identify patterns and predict potential failures before they occur. This transition from reactive to proactive maintenance minimizes downtime, extends equipment lifespan, and significantly lowers operational expenditures, addressing a core concern for businesses with large refrigeration fleets.

Furthermore, AI-powered systems are crucial for enhancing inventory management and ensuring optimal environmental conditions for stored goods. By integrating with existing supply chain and inventory systems, AI can provide real-time insights into stock levels, product freshness, and even consumer demand patterns, allowing for dynamic adjustments to refrigeration settings. This capability is particularly vital for perishable goods, where maintaining precise temperature ranges is critical to preventing spoilage and ensuring food safety. As businesses seek to maximize efficiency and minimize waste, the deployment of AI in commercial refrigeration will become increasingly commonplace, offering a competitive edge through smarter and more sustainable operations.

- Predictive maintenance for reduced downtime and extended equipment life.

- Energy optimization through real-time data analysis and adaptive control.

- Enhanced remote monitoring and fault detection capabilities.

- Improved inventory management and waste reduction for perishable goods.

- Automated diagnostics and troubleshooting, reducing manual intervention.

- Development of self-optimizing refrigeration systems.

Key Takeaways Commercial Refrigeration Equipment Market Size & Forecast

The commercial refrigeration equipment market is poised for robust and sustained growth through 2033, driven primarily by the ongoing expansion of the global food and beverage industry, coupled with increasing urbanization and rising disposable incomes that fuel demand for fresh and processed foods. The forecast indicates that market expansion will be particularly pronounced in emerging economies, where modern retail formats and cold chain logistics are rapidly developing. This growth trajectory underscores the essential role of refrigeration in maintaining food safety, quality, and extending product shelf life across diverse commercial applications, from large supermarkets to small-scale restaurants and industrial food processing units.

A significant takeaway from the market forecast is the pivotal influence of regulatory frameworks and environmental concerns on product innovation and adoption. The global push to phase out high-GWP (Global Warming Potential) refrigerants is accelerating the demand for eco-friendly alternatives such as natural refrigerants (CO2, ammonia, hydrocarbons) and advanced synthetic refrigerants. This regulatory environment, combined with the continuous advancements in energy-efficient technologies, ensures that future market growth will be characterized by smarter, more sustainable, and technologically integrated refrigeration solutions. Businesses that prioritize these innovations are expected to capture a larger share of the expanding market, adapting to both consumer expectations and legislative imperatives.

- Steady growth projected, fueled by global food and beverage sector expansion.

- Significant market opportunities in emerging economies due to infrastructure development.

- Environmental regulations are a key catalyst for adoption of sustainable technologies.

- Technological advancements, including IoT and AI, will redefine operational efficiency.

- Increasing demand for efficient cold chain solutions to minimize food waste.

- Focus on lower operational costs through energy-efficient equipment.

Commercial Refrigeration Equipment Market Drivers Analysis

The global commercial refrigeration equipment market is propelled by several potent drivers, primarily the burgeoning growth of the food and beverage industry worldwide. As populations increase and urbanization accelerates, there is a corresponding surge in demand for perishable goods, necessitating advanced preservation technologies across the supply chain. This includes the expansion of supermarkets, hypermarkets, convenience stores, and specialized food retail outlets, all of which rely heavily on commercial refrigeration to display and store products safely and effectively. Furthermore, the rapid growth of the foodservice sector, encompassing restaurants, cafes, and institutional catering, significantly contributes to the demand for diverse refrigeration units.

Another critical driver is the increasing implementation of stringent food safety regulations and standards across various regions. Governments and regulatory bodies are intensifying efforts to ensure the quality and safety of food products, which mandates the use of reliable and temperature-controlled storage solutions. This push for compliance compels businesses to invest in modern, high-performance refrigeration equipment that meets or exceeds these strict guidelines. Concurrently, technological advancements, such as the integration of smart sensors, IoT connectivity, and energy-efficient compressors, are enhancing the appeal and functionality of new refrigeration systems, driving replacement cycles and new installations as businesses seek to optimize operational costs and reduce environmental impact.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Food Service & Retail Sectors | +1.2% | Global, particularly Asia Pacific & Latin America | Long-term (2025-2033) |

| Growth in Cold Chain Infrastructure | +0.9% | Emerging Economies (India, China, Southeast Asia) | Mid-term (2027-2030) |

| Increasing Focus on Food Safety Regulations | +0.7% | North America, Europe, parts of Asia | Short-term (2025-2027) |

| Technological Advancements in Refrigeration Systems | +0.8% | Globally, led by developed markets | Long-term (2025-2033) |

| Rising Consumer Demand for Fresh & Frozen Foods | +1.0% | Global | Long-term (2025-2033) |

Commercial Refrigeration Equipment Market Restraints Analysis

Despite significant growth prospects, the commercial refrigeration equipment market faces several notable restraints that could temper its expansion. One primary challenge is the high initial capital investment required for purchasing and installing advanced refrigeration systems. Businesses, especially small and medium-sized enterprises (SMEs), may find these upfront costs prohibitive, leading them to either delay upgrades or opt for less efficient, older models. This financial barrier is compounded by the substantial energy consumption associated with refrigeration units, contributing to high operational expenses over the equipment's lifespan. While new energy-efficient models aim to mitigate this, the perceived long-term cost savings may not always outweigh immediate budgetary concerns for all market participants.

Another significant restraint is the ongoing phase-out of traditional refrigerants, particularly hydrofluorocarbons (HFCs), due to their high Global Warming Potential (GWP). While this transition promotes environmental sustainability, it introduces complexities for manufacturers and end-users alike. The development and adoption of alternative, eco-friendly refrigerants often come with higher costs, require specialized training for installation and maintenance, and may necessitate significant infrastructure modifications for existing systems. Furthermore, intense market competition among manufacturers, coupled with price sensitivity from end-users, can exert downward pressure on profit margins, limiting investment in research and development for truly groundbreaking innovations. Supply chain disruptions, often exacerbated by global events, can also hinder production and timely delivery of components, impacting market stability and growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -0.7% | Global, particularly SMEs in developing regions | Long-term (2025-2033) |

| Fluctuating Raw Material & Energy Costs | -0.5% | Global | Short-term (2025-2027) |

| Strict Regulations on Refrigerant Use | -0.6% | Europe, North America, gradually Asia Pacific | Mid-term (2027-2030) |

| Market Saturation in Developed Regions | -0.4% | North America, Western Europe | Long-term (2025-2033) |

| Skilled Labor Shortage for Installation & Maintenance | -0.3% | Global | Mid-term (2027-2030) |

Commercial Refrigeration Equipment Market Opportunities Analysis

The commercial refrigeration equipment market presents substantial opportunities for innovation and growth, primarily driven by the increasing global demand for sustainable and energy-efficient solutions. The growing awareness and stringent regulations concerning climate change are accelerating the adoption of natural refrigerants such as CO2, ammonia, and hydrocarbons, which have minimal environmental impact. This shift opens new avenues for manufacturers to develop and commercialize advanced systems that comply with evolving environmental standards, catering to a market segment increasingly prioritizing ecological responsibility. Moreover, the development of smart and connected refrigeration units, leveraging IoT and AI, represents a significant opportunity. These technologies enable remote monitoring, predictive maintenance, and optimized energy consumption, creating value-added services and operational efficiencies for end-users, fostering a transition towards a service-oriented business model.

Emerging markets, particularly in Asia Pacific, Latin America, and the Middle East & Africa, offer robust growth opportunities due to their rapidly expanding retail and foodservice sectors, coupled with underdeveloped cold chain infrastructure. As these regions experience economic development and urbanization, the demand for modern and efficient commercial refrigeration equipment is set to surge, representing a largely untapped potential. Furthermore, the aging infrastructure in developed markets creates a significant opportunity for retrofitting and upgrading existing refrigeration systems with newer, more energy-efficient, and environmentally compliant technologies. This enables businesses to meet regulatory requirements, reduce operational costs, and enhance performance without entirely replacing their current setups, offering a cost-effective pathway for market penetration and expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Natural & Eco-Friendly Refrigerants | +1.1% | Global, led by Europe & North America | Long-term (2025-2033) |

| Integration of Smart & IoT-Enabled Systems | +0.9% | Developed markets, gradually emerging economies | Long-term (2025-2033) |

| Expansion into Emerging Markets | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Retrofitting & Upgrade of Existing Systems | +0.6% | North America, Europe | Mid-term (2027-2030) |

| Growth in Online Grocery & Food Delivery Services | +0.7% | Global | Mid-term (2027-2030) |

Commercial Refrigeration Equipment Market Challenges Impact Analysis

The commercial refrigeration equipment market is subject to several complex challenges that demand strategic responses from industry players. One significant hurdle is navigating the intricate and constantly evolving landscape of environmental regulations, particularly those pertaining to refrigerant phase-downs and energy efficiency standards. Compliance requires substantial investment in research and development for new technologies and can impose higher manufacturing costs, which may impact product pricing and market competitiveness. Staying abreast of varied regional regulations and ensuring product compliance across different geographies adds a layer of complexity for global manufacturers. Furthermore, rising energy prices globally continue to pose a challenge, as refrigeration units are inherently energy-intensive. This impacts the total cost of ownership for end-users, potentially slowing down investment in new equipment, especially for businesses operating on thin margins.

Another critical challenge is the persistent shortage of skilled labor required for the installation, maintenance, and repair of advanced commercial refrigeration systems. Modern equipment often incorporates complex electronics, IoT capabilities, and utilizes specialized refrigerants, demanding a highly trained workforce. This scarcity can lead to increased service costs, longer repair times, and potential operational inefficiencies for businesses. Moreover, the increasing integration of digital technologies also introduces cybersecurity risks, as networked refrigeration systems become potential targets for malicious attacks, which could compromise data integrity or disrupt critical operations. Addressing these challenges requires continuous investment in training, robust cybersecurity measures, and a proactive approach to regulatory changes to maintain market viability and foster sustainable growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Regulatory Compliance | -0.8% | Global, especially EU & North America | Long-term (2025-2033) |

| Volatile Raw Material Prices | -0.5% | Global | Short-term (2025-2027) |

| High Energy Consumption & Operating Costs | -0.6% | Global | Long-term (2025-2033) |

| Intense Market Competition | -0.4% | Global | Long-term (2025-2033) |

| Cybersecurity Risks with Connected Systems | -0.2% | Developed Markets | Mid-term (2027-2030) |

Commercial Refrigeration Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global commercial refrigeration equipment market, offering detailed insights into market dynamics, segmentation, regional landscapes, and competitive scenarios. It covers the period from 2019 to 2033, including historical data, current market estimations, and future projections. The scope encompasses various product types, applications, refrigerant types, temperature ranges, and capacities, illustrating their respective market contributions and growth trajectories. The report also highlights key market trends, drivers, restraints, opportunities, and challenges influencing the industry, along with a thorough impact analysis of these factors on the market's Compound Annual Growth Rate (CAGR). Furthermore, it provides a comprehensive profile of leading companies, assessing their strategies, product portfolios, and market presence to offer a holistic view of the competitive environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 37.5 Billion |

| Market Forecast in 2033 | USD 63.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Daikin Industries, Ltd., Carrier Corporation, Danfoss A/S, GEA Group AG, Johnson Controls International plc, Emerson Electric Co., Bitzer SE, Illinois Tool Works Inc. (Hobart), Mitsubishi Electric Corporation, Panasonic Corporation, Thermo Fisher Scientific Inc., AHT Cooling Systems GmbH, Whirlpool Corporation, Ali Group S.p.A., True Manufacturing Co., Inc., Fagor Industrial, Hoshizaki Corporation, Manitowoc Company, Inc., Liebherr Group, Arcadia Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The commercial refrigeration equipment market is comprehensively segmented to provide a detailed understanding of its diverse components and their contributions to overall market dynamics. This segmentation facilitates a granular analysis of various market aspects, allowing stakeholders to identify high-growth areas and tailor their strategies effectively. The market is primarily segmented by product type, end-use application, refrigerant type, temperature type, and capacity, each revealing unique demand patterns and technological requirements across different industries and regions. Understanding these distinct segments is crucial for manufacturers to optimize their product offerings, for distributors to refine their sales channels, and for investors to pinpoint promising investment opportunities within the expansive commercial refrigeration landscape.

- Product Type: This segment includes a wide array of equipment such as refrigerators and freezers, display cases, ice machines, beverage coolers, and other specialized refrigeration units. Refrigerators and freezers form the backbone of cold storage, while display cases are vital for retail merchandising.

- End-Use: The market caters to diverse industries including food service (restaurants, cafes, catering), food and beverage retail (supermarkets, hypermarkets, convenience stores, specialty stores), food and beverage production, healthcare (hospitals, pharmacies, laboratories), chemicals and pharmaceuticals, and logistics and transportation, among others. The varying temperature and storage requirements across these sectors drive demand for specific equipment types.

- Refrigerant Type: Segmentation by refrigerant type includes fluorocarbon refrigerants (HFCs, HCFCs), hydrocarbon refrigerants, ammonia refrigerants, and carbon dioxide refrigerants, along with other natural refrigerants. The shift towards low-GWP and natural refrigerants is a significant trend impacting this segment due to environmental regulations.

- Temperature Type: This segment differentiates between medium temperature refrigeration (typically for chilled goods) and low temperature refrigeration (for frozen products). The specific temperature needs dictate the design and technology of the refrigeration units.

- Capacity: Commercial refrigeration equipment is also categorized by capacity into small (below 20 cu. ft.), medium (20-50 cu. ft.), and large (above 50 cu. ft.) units, catering to businesses of varying sizes and operational scales, from small convenience stores to large industrial cold storage facilities.

Regional Highlights

- North America: A mature market characterized by stringent food safety regulations and a high adoption rate of advanced, energy-efficient refrigeration technologies. The region sees significant demand from the foodservice and organized retail sectors, with a growing emphasis on smart refrigeration solutions and natural refrigerants.

- Europe: Driven by strong environmental policies and a focus on sustainability, Europe is a leader in adopting natural refrigerants like CO2 and ammonia. The market is propelled by robust cold chain infrastructure and a well-established food retail sector, with continuous investments in retrofitting older systems for compliance.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid urbanization, expanding disposable incomes, and the proliferation of modern retail formats and foodservice outlets. Significant investments in cold chain development, particularly in countries like China and India, are creating immense opportunities for commercial refrigeration equipment manufacturers.

- Latin America: Experiencing steady growth due to increasing foreign investments in the retail and food processing sectors. The region presents opportunities for both new installations and upgrades, driven by improving economic conditions and a growing preference for processed and frozen foods.

- Middle East and Africa (MEA): This region is witnessing substantial growth in the tourism, hospitality, and food retail sectors, leading to increased demand for commercial refrigeration equipment. Investments in infrastructure development and efforts to diversify economies beyond oil are further contributing to market expansion, particularly in GCC countries and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Refrigeration Equipment Market.- Daikin Industries, Ltd.

- Carrier Corporation

- Danfoss A/S

- GEA Group AG

- Johnson Controls International plc

- Emerson Electric Co.

- Bitzer SE

- Illinois Tool Works Inc. (Hobart)

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Thermo Fisher Scientific Inc.

- AHT Cooling Systems GmbH

- Whirlpool Corporation

- Ali Group S.p.A.

- True Manufacturing Co., Inc.

- Fagor Industrial

- Hoshizaki Corporation

- Manitowoc Company, Inc.

- Liebherr Group

- Arcadia Inc.

Frequently Asked Questions

What is commercial refrigeration equipment?

Commercial refrigeration equipment refers to specialized cooling and freezing units designed for business use, primarily to preserve perishable goods in industries such as food service, retail, healthcare, and logistics. This includes refrigerators, freezers, display cases, ice makers, and beverage coolers.

What types of refrigerants are commonly used in commercial refrigeration?

Historically, HFCs were prevalent, but due to environmental regulations, there's a growing shift towards natural refrigerants like CO2 (carbon dioxide), ammonia (NH3), and hydrocarbons (propane, isobutane), which have lower environmental impacts, alongside newer-generation synthetic refrigerants.

How important is energy efficiency in commercial refrigeration?

Energy efficiency is crucial as refrigeration systems are significant consumers of electricity in commercial settings. Efficient units reduce operational costs, minimize environmental footprint, and help businesses comply with increasingly strict energy consumption regulations.

Which industries are the primary end-users of commercial refrigeration equipment?

The primary end-users include the food service industry (restaurants, cafes, hotels), food and beverage retail (supermarkets, convenience stores), food and beverage production, healthcare (hospitals, pharmacies for medical supplies), and the logistics and transportation sector (cold chain).

What are the future trends shaping the commercial refrigeration market?

Future trends include the pervasive integration of IoT and AI for smart monitoring and predictive maintenance, a continued global transition towards natural and low-GWP refrigerants, increased demand for modular and customized solutions, and the expansion of cold chain infrastructure, particularly in emerging markets.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted