Collaboration Software Market

Collaboration Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702560 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

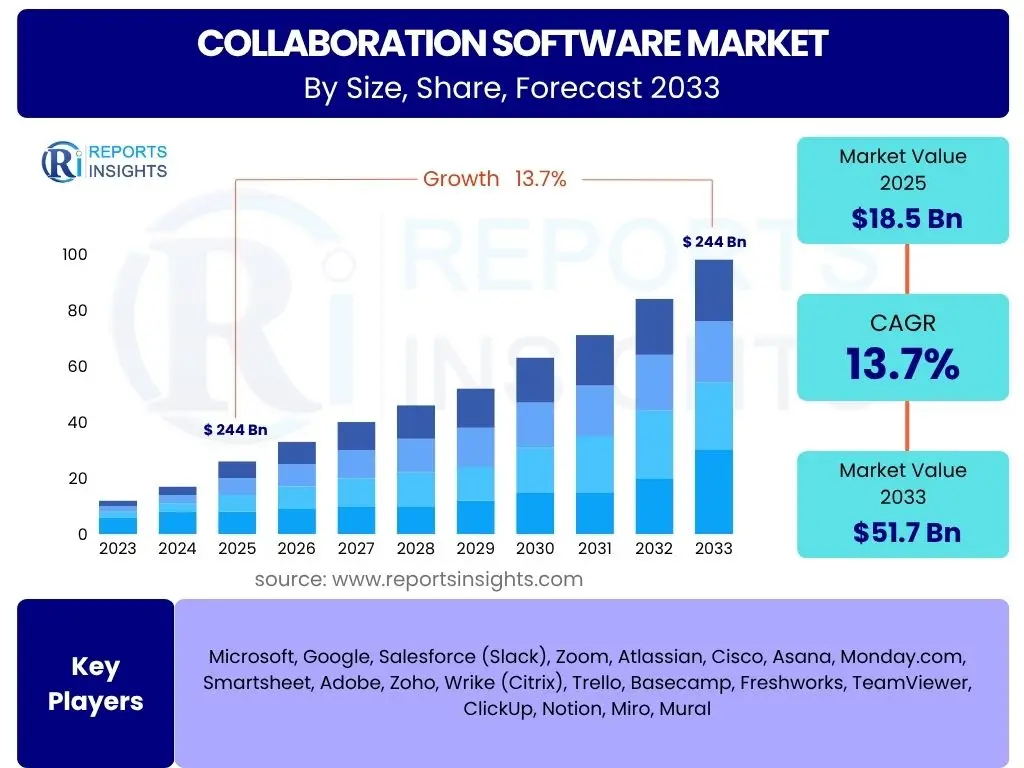

Collaboration Software Market Size

According to Reports Insights Consulting Pvt Ltd, The Collaboration Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 51.7 Billion by the end of the forecast period in 2033.

Key Collaboration Software Market Trends & Insights

User queries frequently center on the evolving landscape of digital teamwork, highlighting a strong interest in how technology facilitates remote and hybrid work models. There is a clear demand for understanding the integration of various communication tools, the increasing importance of security features in shared environments, and the shift towards more intuitive, AI-driven platforms. Furthermore, users are keen to know about the role of mobile accessibility and the convergence of different collaboration functionalities into unified suites, reflecting a desire for seamless and efficient digital workspaces.

The market is experiencing a significant shift towards integrated platforms that offer a comprehensive suite of tools, from communication and project management to document sharing and video conferencing. This integration aims to reduce tool fatigue and enhance workflow efficiency within organizations of all sizes. The proliferation of remote and hybrid work models has undeniably accelerated the adoption of these solutions, making them indispensable for maintaining productivity and connectivity across distributed teams. This trend underscores a fundamental change in how businesses operate, moving beyond traditional office setups.

Another prominent trend involves the growing emphasis on user experience (UX) and intuitive design. Companies are increasingly seeking collaboration tools that are easy to adopt and integrate into existing workflows, minimizing the learning curve for employees. Data security and compliance remain paramount, with businesses prioritizing solutions that offer robust encryption, access controls, and adherence to regional data privacy regulations. This focus on security is critical in an era of heightened cyber threats and increasing regulatory scrutiny, ensuring sensitive information remains protected within collaborative environments.

- Shift to hybrid and remote work models.

- Integration of diverse collaboration functionalities into unified platforms.

- Emphasis on enhanced security features and data privacy compliance.

- Increased adoption of cloud-based collaboration solutions.

- Demand for intuitive user interfaces and seamless user experience.

- Growth of asynchronous communication tools.

- Personalization and customization options for workspaces.

AI Impact Analysis on Collaboration Software

User inquiries regarding the impact of Artificial Intelligence on collaboration software primarily revolve around automation capabilities, intelligent insights, and enhanced user experiences. Common themes include how AI can streamline workflows, automatically summarize meetings, translate languages in real-time, and provide predictive analytics for team productivity. Users are also concerned about data privacy implications and the potential for AI to personalize collaborative environments, while seeking to understand the practical applications that move beyond mere conceptual benefits, focusing on tangible improvements to efficiency and decision-making.

AI is poised to revolutionize collaboration software by automating mundane tasks and offering predictive insights, thereby significantly boosting productivity. Features such as intelligent meeting summaries, automated transcription, and real-time language translation are becoming standard, reducing manual effort and improving communication efficiency across diverse teams. Furthermore, AI-driven analytics can identify bottlenecks in workflows, suggest optimal communication channels, and even predict project delays, enabling proactive intervention and more efficient resource allocation within organizations.

Beyond automation, AI's influence extends to enhancing user experience through personalization and intelligent assistance. AI algorithms can analyze user behavior and preferences to customize interfaces, recommend relevant content, and prioritize notifications, creating a more tailored and less distracting collaborative environment. The integration of virtual assistants and chatbots powered by AI further streamlines interactions, allowing users to quickly access information or perform actions through natural language commands. However, the adoption of AI also raises critical considerations around data security, ethical AI use, and the need for transparent algorithms to maintain user trust and ensure responsible innovation in collaboration tools.

- Automated transcription and intelligent meeting summaries.

- Real-time language translation for global teams.

- AI-driven insights for productivity and workflow optimization.

- Enhanced search capabilities through natural language processing.

- Personalized user experiences and adaptive interfaces.

- Predictive analytics for project management and resource allocation.

- Integration of AI-powered chatbots and virtual assistants.

- Improved data security and anomaly detection.

Key Takeaways Collaboration Software Market Size & Forecast

Common user questions regarding key takeaways from the collaboration software market size and forecast consistently point towards the strategic importance of these tools in modern business operations. Users are keen to understand the projected growth trajectory, the primary drivers fueling this expansion, and the long-term implications for organizational productivity and digital transformation. There is significant interest in identifying which market segments are poised for the most substantial growth and how emerging technologies like AI will influence future market dynamics, all with a view towards making informed investment and adoption decisions.

The collaboration software market is set for substantial growth through 2033, driven by the sustained global shift towards remote and hybrid work models. This fundamental change in work culture necessitates robust digital tools that can connect geographically dispersed teams seamlessly and efficiently. The market's expansion is not merely about communication but encompasses a holistic approach to productivity, project management, and knowledge sharing, making these solutions central to maintaining operational continuity and competitiveness in a dynamic business environment. The increasing complexity of global business operations further underpins this growth, as organizations seek integrated platforms to manage diverse projects and teams.

A key takeaway is the increasing integration of advanced technologies, particularly Artificial Intelligence, which is transforming the capabilities of collaboration platforms. AI-driven features are moving beyond simple automation to offer intelligent insights, personalized experiences, and predictive functionalities that enhance decision-making and workflow efficiency. This technological evolution is not only attracting new users but also encouraging existing users to upgrade to more sophisticated solutions, thereby contributing significantly to market value. Furthermore, the market will increasingly be characterized by solutions that prioritize user experience, security, and scalability, addressing the evolving needs of both small businesses and large enterprises across various industries.

- Sustained growth driven by remote and hybrid work adoption.

- Significant market expansion expected to reach USD 51.7 Billion by 2033.

- AI integration is a major catalyst for innovation and value creation.

- Cloud-based solutions will continue to dominate, offering scalability and accessibility.

- Emphasis on integrated platforms that offer end-to-end solutions.

- Robust demand from Small & Medium Enterprises (SMEs) and large enterprises.

- Cybersecurity and data compliance remain critical differentiators.

Collaboration Software Market Drivers Analysis

The collaboration software market is experiencing robust growth fueled by several key drivers. The most prominent among these is the widespread adoption of remote and hybrid work models, which have made digital collaboration tools indispensable for maintaining productivity and communication across distributed teams. This paradigm shift in work culture has necessitated a fundamental change in how businesses operate, with collaboration software becoming a core component of daily operations. Beyond remote work, the increasing globalization of businesses means teams are often spread across different geographies and time zones, demanding sophisticated tools that can bridge these distances and facilitate seamless interaction.

Another significant driver is the continuous advancement in technology, particularly the integration of Artificial Intelligence and machine learning capabilities into collaboration platforms. These technologies enable features such as intelligent automation, enhanced analytics, and personalized user experiences, making collaboration tools more efficient and intuitive. Furthermore, the growing demand for improved efficiency and productivity across all organizational levels is pushing companies to invest in solutions that streamline workflows, reduce manual tasks, and optimize resource allocation. The need for better project management, real-time document sharing, and seamless communication channels also acts as a strong impetus for market expansion. Lastly, the rise of cloud computing offers scalability, accessibility, and cost-effectiveness, further accelerating the adoption of cloud-based collaboration software.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Proliferation of Remote & Hybrid Work Models | +3.5% | Global, particularly North America, Europe, APAC | Short to Long-term (2025-2033) |

| Increasing Demand for Enhanced Productivity and Efficiency | +2.8% | Global, across all industries | Short to Mid-term (2025-2030) |

| Technological Advancements (AI, Cloud Computing) | +2.5% | Global, especially developed economies | Mid to Long-term (2027-2033) |

| Growing Need for Seamless Communication and Information Sharing | +1.9% | Global, cross-industry | Short to Mid-term (2025-2030) |

| Digital Transformation Initiatives Across Enterprises | +1.5% | Global, especially large enterprises | Mid to Long-term (2026-2033) |

Collaboration Software Market Restraints Analysis

Despite the robust growth, the collaboration software market faces several significant restraints that could impede its full potential. A primary concern for organizations is data security and privacy. With sensitive company information being shared and stored on these platforms, breaches and unauthorized access pose substantial risks, leading to hesitancy in widespread adoption, especially among highly regulated industries. This concern is often amplified by the complexity of adhering to various global and regional data protection regulations, such as GDPR and CCPA, which require sophisticated compliance measures from software providers.

Another notable restraint is the high cost of implementation and subscription fees, particularly for comprehensive enterprise-grade solutions. While basic versions may be affordable, advanced features, scalability for large user bases, and extensive customization can become prohibitively expensive, deterring Small and Medium-sized Enterprises (SMEs) or organizations with limited IT budgets. Furthermore, the steep learning curve associated with complex software and the challenges of integrating new collaboration tools with existing legacy systems can create significant friction. This integration complexity often leads to resistance from employees accustomed to traditional workflows, requiring extensive training and change management efforts that add to the overall cost and time of deployment, thus slowing down adoption rates across the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -1.8% | Global, particularly Europe (GDPR) and North America | Long-term (Ongoing) |

| High Cost of Implementation and Subscription | -1.5% | Global, especially SMEs and developing regions | Short to Mid-term (2025-2030) |

| Integration Complexities with Legacy Systems | -1.2% | Global, large enterprises with established IT infrastructure | Mid-term (2026-2031) |

| Employee Resistance to Change and Adoption Challenges | -0.8% | Global, varying by organizational culture | Short-term (2025-2027) |

| Interoperability Issues Among Diverse Platforms | -0.7% | Global, cross-industry | Short to Mid-term (2025-2029) |

Collaboration Software Market Opportunities Analysis

The collaboration software market presents numerous opportunities for growth and innovation, driven by evolving work environments and technological advancements. A significant opportunity lies in the expanding adoption of hybrid work models globally, which necessitates more flexible and robust collaboration solutions that can seamlessly connect employees working from various locations. This trend is not confined to large enterprises but extends to Small and Medium-sized Enterprises (SMEs) that are increasingly recognizing the value of digital tools for productivity and remote operations, representing a largely untapped segment with significant growth potential for providers offering scalable and affordable solutions tailored to their specific needs.

Another major opportunity stems from the continuous integration of emerging technologies like Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Things (IoT) into collaboration platforms. These integrations enable advanced functionalities such as intelligent automation, predictive analytics for team performance, real-time language translation, and enhanced security measures, creating significant value for users. The vertical-specific customization of collaboration tools also offers a lucrative avenue, as industries like healthcare, education, and finance require tailored solutions that address their unique regulatory and operational needs. Furthermore, the growing emphasis on employee engagement and well-being, even in remote settings, creates demand for platforms that offer features beyond basic communication, such as virtual team-building activities, mental health resources, and personalized productivity insights, thereby fostering a more connected and supportive digital workplace.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Untapped SME Market Segments | +2.3% | Global, particularly emerging economies and underserved regions | Short to Mid-term (2025-2030) |

| Integration of Advanced Technologies (AI, ML, IoT) | +2.0% | Global, particularly tech-forward regions (North America, Europe, APAC) | Mid to Long-term (2027-2033) |

| Development of Niche, Industry-Specific Solutions | +1.7% | Global, varying by industry concentration in regions | Mid-term (2026-2031) |

| Demand for Unified Communication & Collaboration (UCC) Suites | +1.5% | Global, across large and medium enterprises | Short to Mid-term (2025-2029) |

| Increasing Focus on Employee Experience and Wellbeing Features | +1.0% | Global, especially developed markets | Mid-term (2027-2032) |

Collaboration Software Market Challenges Impact Analysis

The collaboration software market, while booming, faces several significant challenges that could hinder its sustained growth and widespread adoption. One primary challenge is the intense competition among a multitude of providers, ranging from established tech giants to agile startups. This crowded landscape often leads to price wars, feature parity, and difficulty in differentiating offerings, making it challenging for new entrants to gain traction and for existing players to maintain market share without constant innovation. This competitive pressure can also impact profitability and force companies to continuously invest heavily in research and development to stay relevant.

Another substantial challenge lies in ensuring robust data security and privacy compliance across diverse regulatory environments. As collaboration tools handle vast amounts of sensitive organizational data, breaches or non-compliance with regulations like GDPR, CCPA, or industry-specific standards can lead to severe financial penalties, reputational damage, and loss of user trust. Furthermore, user adoption and change management present ongoing hurdles. Despite the benefits, employees may resist adopting new tools due to unfamiliarity, perceived complexity, or preference for established workflows. Overcoming this resistance requires comprehensive training, intuitive design, and strong leadership buy-in, adding a layer of complexity to deployment and long-term user engagement. Finally, interoperability issues between different platforms and legacy systems can create fragmented workflows, reducing the overall efficiency that collaboration software aims to deliver.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Market Saturation | -1.6% | Global, especially North America and Europe | Long-term (Ongoing) |

| Maintaining Data Security & Regulatory Compliance | -1.4% | Global, highly regulated industries (BFSI, Healthcare) | Long-term (Ongoing) |

| User Adoption and Effective Change Management | -1.0% | Global, varying by organizational culture | Short to Mid-term (2025-2028) |

| Integration with Existing Legacy Systems | -0.9% | Global, particularly large, established enterprises | Mid-term (2026-2030) |

| Managing Tool Sprawl and Interoperability | -0.6% | Global, increasing with diverse software portfolios | Short to Mid-term (2025-2029) |

Collaboration Software Market - Updated Report Scope

This report provides a comprehensive analysis of the global Collaboration Software Market, encompassing market sizing, growth forecasts, and in-depth insights into key trends, drivers, restraints, opportunities, and challenges influencing the industry. It segments the market by component, deployment, organization size, industry vertical, and regional presence, offering a granular view of market dynamics. The scope also includes an extensive competitive landscape analysis, profiling key players and their strategic initiatives. Furthermore, the report delves into the impact of emerging technologies like Artificial Intelligence on market evolution, providing a strategic roadmap for stakeholders to navigate future market developments and capitalize on growth opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 51.7 Billion |

| Growth Rate | 13.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Microsoft, Google, Salesforce (Slack), Zoom, Atlassian, Cisco, Asana, Monday.com, Smartsheet, Adobe, Zoho, Wrike (Citrix), Trello, Basecamp, Freshworks, TeamViewer, ClickUp, Notion, Miro, Mural |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The collaboration software market is broadly segmented to provide a detailed understanding of its diverse applications and user base. These segmentations are crucial for identifying specific growth pockets and tailoring solutions to meet varied organizational needs. The market is primarily categorized by component, deployment model, organization size, and industry vertical, each revealing unique demand patterns and adoption trends. This multi-dimensional segmentation allows for a comprehensive analysis of market dynamics, helping stakeholders identify lucrative opportunities and develop targeted strategies for market penetration and expansion across different sectors.

The "Component" segment differentiates between standalone solutions (such as conferencing tools, messaging applications, project management platforms, and document sharing services) and the ancillary services (including consulting, integration, and support & maintenance) that ensure the effective deployment and utilization of these solutions. The "Deployment" segment highlights the preference for cloud-based, on-premise, or hybrid models, reflecting varying organizational needs for accessibility, security, and control. "Organization Size" distinguishes between the requirements of Small & Medium Enterprises (SMEs), which often prioritize cost-effectiveness and ease of use, and Large Enterprises, which demand robust, scalable, and highly customizable solutions with advanced security features. Lastly, the "Industry Vertical" segmentation recognizes the unique operational and regulatory demands of sectors like IT & Telecom, BFSI, Healthcare, and Education, leading to specialized collaboration tool development tailored to specific industry workflows and compliance requirements.

- By Component:

- Solutions:

- Conferencing (Video, Audio)

- Messaging (Instant Messaging, Team Chat)

- Project Management (Task Management, Workflow Automation)

- Document Sharing & Sync (File Sharing, Co-editing)

- Others (Whiteboarding, Polling, etc.)

- Services:

- Consulting Services

- Integration Services

- Support & Maintenance Services

- Solutions:

- By Deployment:

- Cloud-based

- On-premise

- Hybrid

- By Organization Size:

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical:

- IT & Telecom

- BFSI (Banking, Financial Services & Insurance)

- Healthcare & Life Sciences

- Retail & E-commerce

- Education

- Government & Public Sector

- Media & Entertainment

- Manufacturing

- Others (Legal, Consulting, etc.)

Regional Highlights

The global collaboration software market exhibits distinct regional dynamics, influenced by factors such as technological adoption rates, economic development, prevalence of remote work, and regulatory landscapes. North America consistently holds the largest market share, driven by a high concentration of technology companies, widespread adoption of cloud-based solutions, and a culture that rapidly embraces digital transformation. The region benefits from significant investments in advanced IT infrastructure and a large number of enterprises that are early adopters of innovative collaboration tools, particularly those incorporating AI and unified communication features. The presence of major market players and a mature IT ecosystem further solidify North America's leading position in the collaboration software market.

Europe represents another significant market, characterized by strong regulatory frameworks concerning data privacy (e.g., GDPR) which influence software development, and a growing emphasis on hybrid work models. The Asia Pacific (APAC) region is projected to be the fastest-growing market due to rapid digitalization initiatives, increasing internet penetration, a burgeoning SME sector, and a large, tech-savvy young workforce. Countries like China, India, Japan, and Australia are experiencing substantial growth in demand for collaboration tools as businesses expand and modernize their operations. Latin America and the Middle East & Africa (MEA) are emerging markets, showing increasing adoption fueled by digital transformation efforts, improved connectivity, and a growing awareness of the benefits of streamlined digital workflows, albeit from a smaller base compared to more developed regions.

- North America: Dominant market share due to early technology adoption, strong IT infrastructure, high presence of key market players, and widespread embrace of hybrid work. Significant R&D investments.

- Europe: Mature market with strong growth driven by digitalization, strict data privacy regulations (GDPR) influencing product development, and a focus on integrated, secure collaboration solutions. Germany, UK, and France are key contributors.

- Asia Pacific (APAC): Fastest-growing region, fueled by rapid digital transformation, increasing internet penetration, burgeoning SME sector, and a large mobile-first user base. China, India, Japan, and Australia are major growth engines.

- Latin America: Emerging market with increasing adoption spurred by economic development, growing internet connectivity, and the need for efficient remote work solutions in various industries. Brazil and Mexico lead the adoption.

- Middle East & Africa (MEA): Developing market driven by government initiatives for smart cities, diversification of economies, and increasing investments in IT infrastructure, particularly in the UAE, Saudi Arabia, and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Collaboration Software Market.- Microsoft Corporation

- Google LLC

- Salesforce.com, Inc. (Slack Technologies)

- Zoom Video Communications, Inc.

- Atlassian Corporation Plc

- Cisco Systems, Inc.

- Asana, Inc.

- Monday.com Ltd.

- Smartsheet Inc.

- Adobe Inc.

- Zoho Corporation Pvt. Ltd.

- Citrix Systems, Inc. (Wrike)

- Trello (an Atlassian company)

- Basecamp (37signals)

- Freshworks Inc.

- TeamViewer AG

- ClickUp

- Notion Labs, Inc.

- Miro

- Mural

Frequently Asked Questions

Analyze common user questions about the Collaboration Software market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is collaboration software?

Collaboration software is a suite of digital tools designed to facilitate communication, coordination, and project management among individuals and teams, enabling them to work together effectively regardless of their physical location. It encompasses features like messaging, video conferencing, document sharing, task management, and online whiteboards.

What are the primary benefits of using collaboration software?

The primary benefits include enhanced team productivity, improved communication efficiency, streamlined project workflows, increased flexibility for remote and hybrid work models, better knowledge sharing, and reduced operational costs associated with traditional office setups.

How is AI impacting collaboration software?

AI is significantly impacting collaboration software by enabling features such as automated meeting summaries, real-time language translation, intelligent scheduling, personalized content recommendations, and predictive analytics for team performance, ultimately boosting efficiency and user experience.

What are the key challenges in adopting collaboration software?

Key challenges include ensuring data security and privacy, managing the high cost of enterprise-grade solutions, integrating with existing legacy systems, overcoming employee resistance to new tools, and navigating the complexities of tool sprawl and interoperability issues.

Which industries are adopting collaboration software the most?

Industries showing the highest adoption include IT & Telecom, BFSI, Healthcare, Retail & E-commerce, and Education. These sectors increasingly rely on digital tools for seamless communication, project management, and operational efficiency, especially with the rise of remote and hybrid work models.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted